the divisional budget, divisional goals and

objectives, and different types of budgeting.

THE BUDGET PROCESS

The budget process starts when the President

submits his budget to Congress in mid-January.

Congress can accept the budget as is, or make

changes to the budget through a series of Con-

gressional committees. Congress develops a

budget resolution or an outline of the budget with

spending targets set. Next, Congress passes an

authorization bill which gives authorization to the

various programs in the budget. Still, no money

has been allocated. Money is allocated by the

appropriations bill. The appropriations bill gives

money to the various programs authorized under

the authorizations bill. Once given both authoriza-

tion and appropriations, the Navy can begin to

spend money. Sometimes Congress will authorize

a program but not provide appropriations.

Congress can also provide appropriations but not

authorize the program. The Navy’s A-6F Intruder

is an example of a program that was appropriated

but not authorized.

The next step in the budget process is called

execution. Execution is when the Navy can actually

spend money. During execution, apportionment

takes place. Apportionment is when the Office of

Management and Budget (OMB) places the Con-

gressionally appropriated funds into the Navy’s

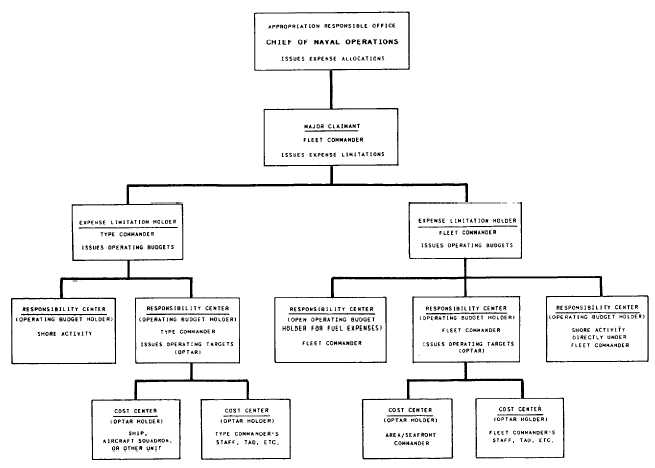

account. See figure 4-1 for the fund flow of the

operation and maintenance account.

The cost center or operating target (OPTAR)

holder at the bottom of figure 4-1 is your ship,

squadron, or unit. Your commanding officer is

responsible for ensuring the OPTAR is met. He

also must make periodic reports to the type

commander showing the status of the ship or unit

funds.

The Navy recognizes that commanding

officers need help in administering their budget.

Comptrollers or budget administrators, depending

on the size of the command, are assigned to assist

Figure 4-1.-Fund flow for operation and maintenance.

4-2